Overview

Three and a half days after it convened, the Colorado Legislature ended its special session on property tax. The session was called in response to a dramatic increase in property taxes that both residential and commercial property owners have experienced over the last two years and to forestall more draconian tax-cut measures on the November ballot that would have left the state responsible for billions in backfill funding.

The special session was not the first attempt by the legislature to address these issues this year. The regular legislative session ended in May with the passage of SB24-233, which was passed in an proactive effort to head off Initiatives 50 and 108 at the ballot in November. The hope was that by passing SB 233, the proponents of Initiatives 50 and 108 would withdraw their measures from the ballot. However, the property tax relief put forward in in SB 233 was insufficient to convince the backers of the initiatives to remove their measures from the ballot.

After negotiating the elements of a compromise with the ballot measure proponents this summer, the governor called for the legislature to return for a special session for the purpose of passing a bill that would supplant both SB 233 and Initiatives 50 and 108.

When the legislature convened, 13 bills were introduced but only two made it across the finish line and to the desk of the governor: HB24B-1001, which is the compromise bill and provides deeper property tax relief than SB 233 but not as much relief as the ballot measures; and HB24B-1003, which provides additional and permanent property tax relief to those owning controlled environment agriculture and greenhouse equipment.

True to the deal, the proponents have agreed to submit their letters of withdrawal for Initiatives 50 and 108 to the secretary of state to remove them from the ballot contemporaneously with the governor signing HB 1001 into law.

What’s in the compromise bill?

Although HB 1001 has the same “cut and cap” components contained in SB 233 and Initiatives 50 and 108, it does not require the state to backfill local districts for lost revenue. Removal of the local backfill was critical to the deal given fiscal estimates that put Initiative 108’s cost to the state at $2.4 billion.

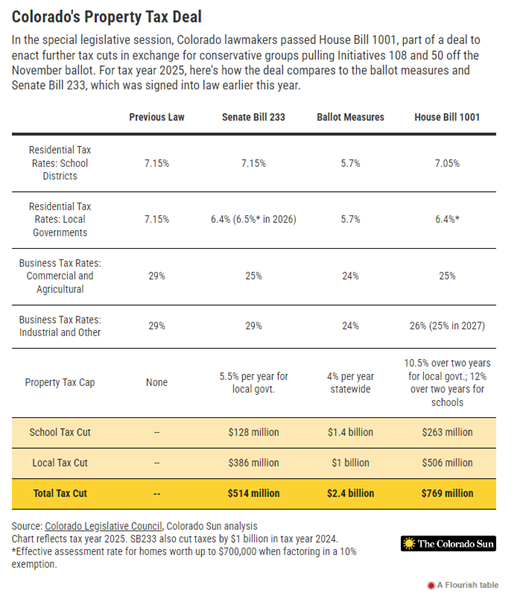

For its part, HB 1001 reduces assessment rates for most residential and nonresidential property over the next few years. Most nonresidential property (commercial, industrial, and agricultural) will see a reduction in assessment rate from 29% to 25% by 2027. Residential assessment rates will be separated for local governments and school districts, with the effective local government residential assessment rate going from 7.15% to 6.4% and the effective school district residential assessment rate going from 7.15% to 7.05%.

In addition to the reduction in assessment rates, HB 1001 imposes a cap on the amount of year-over-year increase in property tax revenue that local governments and school districts can take in. Under the bill, property tax revenue for local governments can grow by no more than 5.25% per year, while revenue for school districts can grow by no more than 6% per year. Those limits are blunted, however, by an amendment that was added to the bill allowing local governments and school districts to “rollover” any unused portion of their property tax revenue cap from one assessment cycle to the next. For example, this means that if property values increase by 8% in one cycle, but a school district’s cap is 12%, the district can carry over the unused 4% to the next cycle. This would give the district a 16% cap for the following assessment cycle. The bill also gives local governments and school districts the authority to go before local voters for permission to keep property tax revenues in excess of their cap.

The following chart, compiled by the The Colorado Sun, shows that HB 1001 will ultimately save property owners $769 million in property taxes for 2025, as comparted to the $2.4 billion impact of Initiatives 50 and 108 and SB 233’s $514 million in savings:

What happened?

As was widely reported before the start of the special session, a resolution sponsored by Rep. Weissman and Sen. Hansen was introduced in order to refer to the voters a constitutional amendment restricting future statewide property tax ballot measures. Republicans indicated from the outset that the resolution would be a dealbreaker. While the proposal passed the House, the sponsors ultimately withdrew it during its Senate committee hearing after it had become clear that the two-thirds votes needed to pass the resolution on the Senate floor were not there.

From the first House committee, rank-and-file legislators voiced displeasure with the compromise legislation, expressing frustration at being called in to rubber stamp a deal that they were not involved in negotiating.

In terms of witness testimony, Colorado’s fire districts were notable in not only calling attention to the impact of HB 1001 on their budgets, but also noting the additional, outlying budget challenges they face as the state continues to see a sharp increase in wildfires and other natural disasters requiring critical emergency response. Also noteworthy was the united front of Colorado’s educational bodies. Many K-12 and all of Colorado’s higher educational institutions testified in support of HB 1001. They expressed concern that should Initiatives 50 and 108 pass, the burden of the state backfilling the tax cuts would affect their ability to provide quality education.

Despite these debates, it was clear that while there was disagreement over whether additional property tax relief is needed, there was alignment on the risk of the measures going to the ballot in November and the detrimental effects it would have on state funding of myriad programs. Ultimately, HB 1001 passed the legislature on a collective vote of 75-22, with three members excused across both chambers.

What’s next?

The deadline to withdraw initiatives from the ballot is Sept. 6, and the governor has indicated that he will not sign the compromise bill into law unless the ballot measures are withdrawn. Our understanding is the proponents of Initiatives 50 and 108 will submit the required withdrawal letter to the secretary of state, after which the governor will sign the bill into law.

This document is intended to provide you with general information regarding the recent Colorado special legislative session. The contents of this document are not intended to provide specific legal advice. If you have any questions about the contents of this document or if you need legal advice as to an issue, please contact the attorneys listed or your regular Brownstein Hyatt Farber Schreck, LLP attorney. This communication may be considered advertising in some jurisdictions. The information in this article is accurate as of the publication date. Because the law in this area is changing rapidly, and insights are not automatically updated, continued accuracy cannot be guaranteed.